The 101 on Assume Balance

It's tempting to buy an assume balance car. But buyer beware, you can land in legal trouble if you miss a few details.

In the last few years, there has been a common sight on online car clubs and groups: it's called 'assume balance'.

What is this rather unusual automobile-related transaction? More importantly, is it worth considering whether you're the one selling or the one buying?

What is Assume Balance?

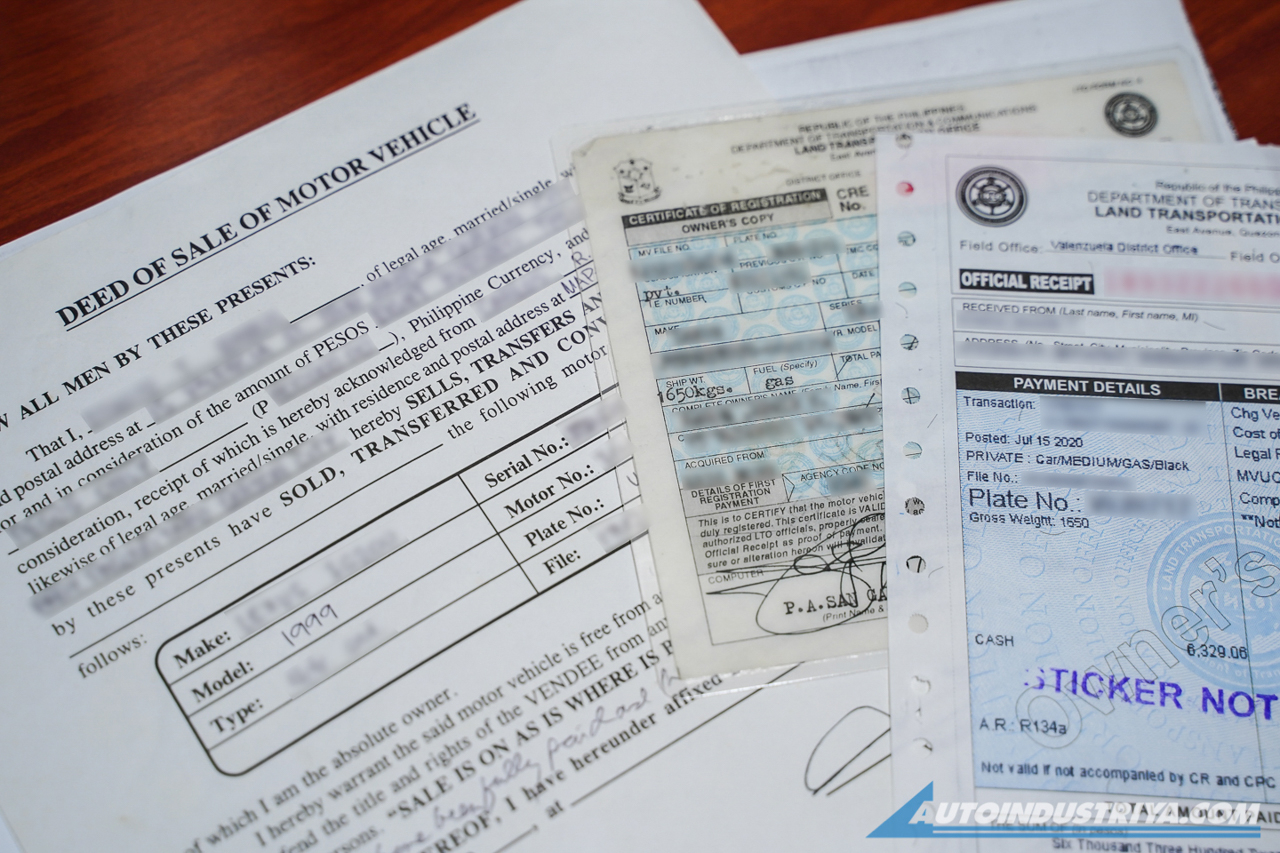

'Assume balance,' also known colloquially as 'pasalo', is when a vehicle that is still in the middle of its term loan, is sold by the lendee (the person to whom the bank gave the original auto loan). The buyer then takes over the auto loan and pays the balance to the bank based on the repayment schedule.

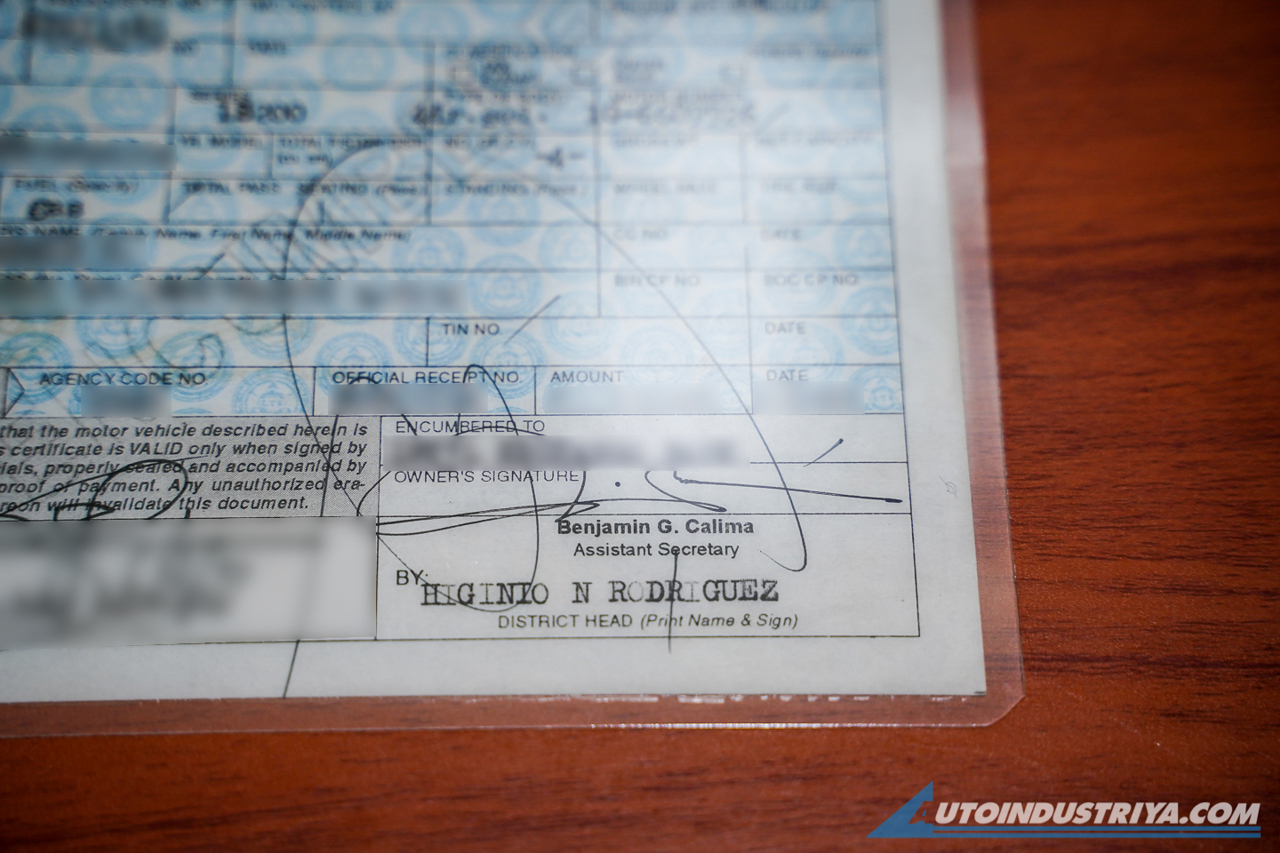

It has become common practice despite the fact auto loans per se, are not assumable, which makes any transaction of the sort technically illegal.

For sellers

If you need to get rid of your auto loan mid-term because you can’t afford the monthly payments anymore, you can either return the vehicle to the lender or sell it as ‘assume balance.’

If A is not an option for you (thinking of all the monthly payments going down the drain gives you heartburn), you can do B. However, that will be contingent on bank approval, and know that there will be risks.

Per a retired executive, “some (financial institutions) may allow and some won’t.”.

The responsibility of seeking permission falls on you, the lendee. If the bank allows it, the buyer is subject to the same credit investigation process. They also need to submit the same documents required of the original borrower.

Once the bank gives consent and everything is above board, there’s good news for everyone. You’re mortgage-free, and the buyer’s principal amount will surely be much lower than what you used to pay.

It would be in the interest of both seller and buyer to secure their copies of the bank’s written consent because 2017 was notorious for ‘assume balance’ cases where banks repo’d vehicles weeks after the buyers ‘paid’ for them. As it turns out, sellers who were about to default on their loans opted to sell their cars instead of returning the unit to the bank.

But what if the bank says no? Should you still go ahead and sell the vehicle? You can, but know that this transaction can go sideways in so many ways.

As a seller, you risk a lot more. The bank can sue you criminally for selling and removing the vehicle from your premises without their consent because it breaches the Chattel Mortgage agreement, and you’ll be the one that ends up with a bad credit rating if the buyer fails to make the monthly payments.

Should the buyer renege on the amortization, the bank will go after the seller to foreclose the mortgage and to repossess the vehicle. That's because the sale didn’t have the consent of the lending institution. As the seller, all you can do is to demand that the buyer pays the mortgage or request for the immediate cancellation of the Deed of Absolute Sale. With that, the vehicle can be returned to you, for turnover to the bank.

If the buyer won’t comply, plead and beg because the alternative, a lawsuit, will take very long and be very expensive.

Whatever you do, DO NOT play repo man and try to personally take the vehicle away from the buyer. Remember, you signed your rights away in the Deed of Absolute Sale. You will be in a tough spot because you’re still legally obligated to pay for a vehicle that you no longer legally own. That said, you can do that IF you made them sign a Chattel Mortgage in your favor.

For Buyers

Buyer, here’s your situation. Without the bank’s consent, the vehicle can’t legally be sold to you. You may execute a Deed of Absolute Sale to protect your purchase but make sure it specifies that the vehicle is still mortgaged to the bank and indicate the terms of payment. That will help you keep ownership of the unit, subject to the bank mortgage, which means you’ll take over the seller’s remaining balance with the lender.

If possible, arrange to pay the bank directly instead of sending monthly checks to the seller. This way, your purchase isn’t dependent on the diligence or delinquency of the seller.

Now, let’s see if this vehicle is worth all of the hassle.

If the unit is still under warranty, that’s a big thumbs up. At least buyers are assured that if a component fails due to ‘material fault’ (break downs without outside influence), it will be replaced free-of-charge. Of course, the warranty does not cover consumable parts like brake pads, air cleaner, oil filter, etc. Also, ask for the service record of the vehicle from the dealership that released the unit.

On the vehicle itself, here’s what buyers should check:

-Check the tires for tread wear. Whip out a small ruler and see if the tread is at least 1.8 mm deep. Otherwise, haggle for a new set.

-If it has a manual transmission and the mileage is under 20,000 kilometers, the gearbox should be ok. Get a mechanic to check if the vehicle is around four years old or has run more than 80,000 kilometers.

-ATs are tougher unless used as TNVS (transport network vehicle service, like Grab). A three to five-year-old unit should be okay.

-Alternator and compressor drive belts need to be replaced every 60,000 kilometers or three years, whichever comes first. Timing belts only last for 80,000 kilometers, while timing chains can go for at least 100,000 kilometers.

-Brake pads on ATs should be changed after 20,000 kilometers; MTs at 40,000 kilometers.

-Drive the vehicle over humps. If the shock absorbers bottom out on exit, you’re going to need a new set.

-Vibrations and faint rattling through the steering wheel may mean a tie rod or rack end problem. Have it thoroughly checked.

-If you hear squeaking or knocking sounds, the bushings may be asking for a replacement.

A note to sellers

It makes no sense to stay on a loan you can’t afford. If you’re in this position right now, get in touch with your bank ASAP and find the easiest and least costly arrangement. Remember, the bank doesn’t want to repossess the unit because it's a loss for them. They want (monthly) payments, and if you don’t have it but give them a good enough explanation, they might allow you to find somebody who does.

Just don’t forget the basic legal jargon above and remember to go through all the necessary steps to avoid becoming a target of legal action.

You’ll be dealing with banks, so this is not one of those times to fake it ‘til you make it. Make sure to dot all the i’s and cross all the t’s because you know what they say, to ‘assume’ makes an ass of u and me.

Related Posts

Barely Legal Speed: The Ariel Atom 4RR and its insane power-to-weight ratio

Built to celebrate 25 years of the Atom, the 4RR is the quickest and most powerful production Atom in the model’s history.

MIAS 2026: A shopper's delight for parts, accessories, and tools

The aftermarket section at MIAS showcases options for car enthusiasts to personalize, enhance, and maintain their vehicles

MIAS 2026: What we saw at the Classic and Custom Car Competition

We take a look at some of the entries at this year's MIAS Classic and Custom Car Competition

Six things to plan ahead for 2026 Manila International Auto Show

Heading to the 2026 Manila International Auto Show? Here are some tips to make sure you maximize the experience at World Trade Center

First Impressions: Did 2026 Nissan Kicks e-Power get the right updates?

Did Nissan do enough to keep the Kicks e-Power competitive in the hybrid crossover segment with its new update?

2026 Toyota RAV4 HEV: The promised hybrid?

Is the all-new sixth-generation Toyota RAV4 HEV worth it at a starting price of PHP 2.183M?